For decades, the covenant between private equity firms and institutional investors was simple: lock up capital for ten years, endure illiquidity, and receive returns that comfortably eclipse the public markets. During the boom years between 1995 and 2000, and again following the dot-com collapse, the industry delivered on this promise. But the math has changed. Since 2006, private equity returns have largely tracked the S&P 500, and recent performance suggests the premium has evaporated entirely.

According to MSCI, between 2022 and the third quarter of 2025, an index of U.S. private equity funds generated annualized returns of just 5.8 percent. Over the same period, the S&P 500 delivered 11.6 percent. Even using the industry’s preferred and often criticized internal rate of return (IRR) metric, the public index outperformed the median private equity fund over the five years ending in 2024.

This underperformance is merely the surface symptom of a deeper structural malaise. The industry is currently paralyzed by a valuation disconnect and a historic exit drought, leaving it sitting on an inventory of 31,000 unsold companies valued at $3.7 trillion. As distributions dry up and "zombie" assets accumulate, the sector faces a reckoning that financial engineering can no longer disguise.

The roots of the current stagnation lie in the market correction of 2022. When the S&P 500 fell by nearly 20 percent, private equity general partners (GPs) did not mark their portfolios to market. Relying on internal valuation models rather than public trading prices, managers insisted their portfolio companies were insulated from the downturn.

This refusal to reset valuations created a persistent pricing gap between buyers and sellers. Compounded by the Federal Reserve raising interest rates by 5.25 percent between March 2022 and July 2023, the era of cheap leverage that fueled acquisitions between 2010 and 2021 came to an abrupt halt. The result has been a seizure in exit activity.

Data from The Wall Street Journal illustrates the severity of the decline. From a peak of 1,210 exits in 2021, activity plummeted to 658 in 2022 and further to 323 in 2023. While 2025 saw a slight recovery in exit value to $243.9 billion driven largely by outliers like the $6.26 billion Medline IPO, the number of exits remained depressed at 321 as of late December. The mechanism that historically returned cash to pension funds and endowments has stalled, forcing holding periods to stretch from the traditional 10 years to 12 or even 15 years.

.png)

As exits stall, "zombie funds," defined as investment vehicles 10 years or older that have not liquidated their assets are accumulating at a record pace. For funds based in North America, assets under management in these stagnant vehicles grew from $372 billion in 2021 to a record $441 billion in 2024.

This is not a problem confined to niche players; the majority of these unsold assets reside in large funds ($1 billion to $5 billion) managed by established firms. The vintage year 2014 serves as a stark warning: ten years after launch, a worrying 77 percent of the capital raised by these funds remained unrealized in 2024.

For limited partners (LPs), the economic implications of zombie assets are deteriorating. Historically, such funds returned 53 cents on the dollar for remaining assets. Today, that recovery rate has dropped to 44 cents. Despite this, firms continue to collect management fees on these aging portfolios, creating a misalignment of incentives where GPs are paid to hold assets they cannot sell at their book value.

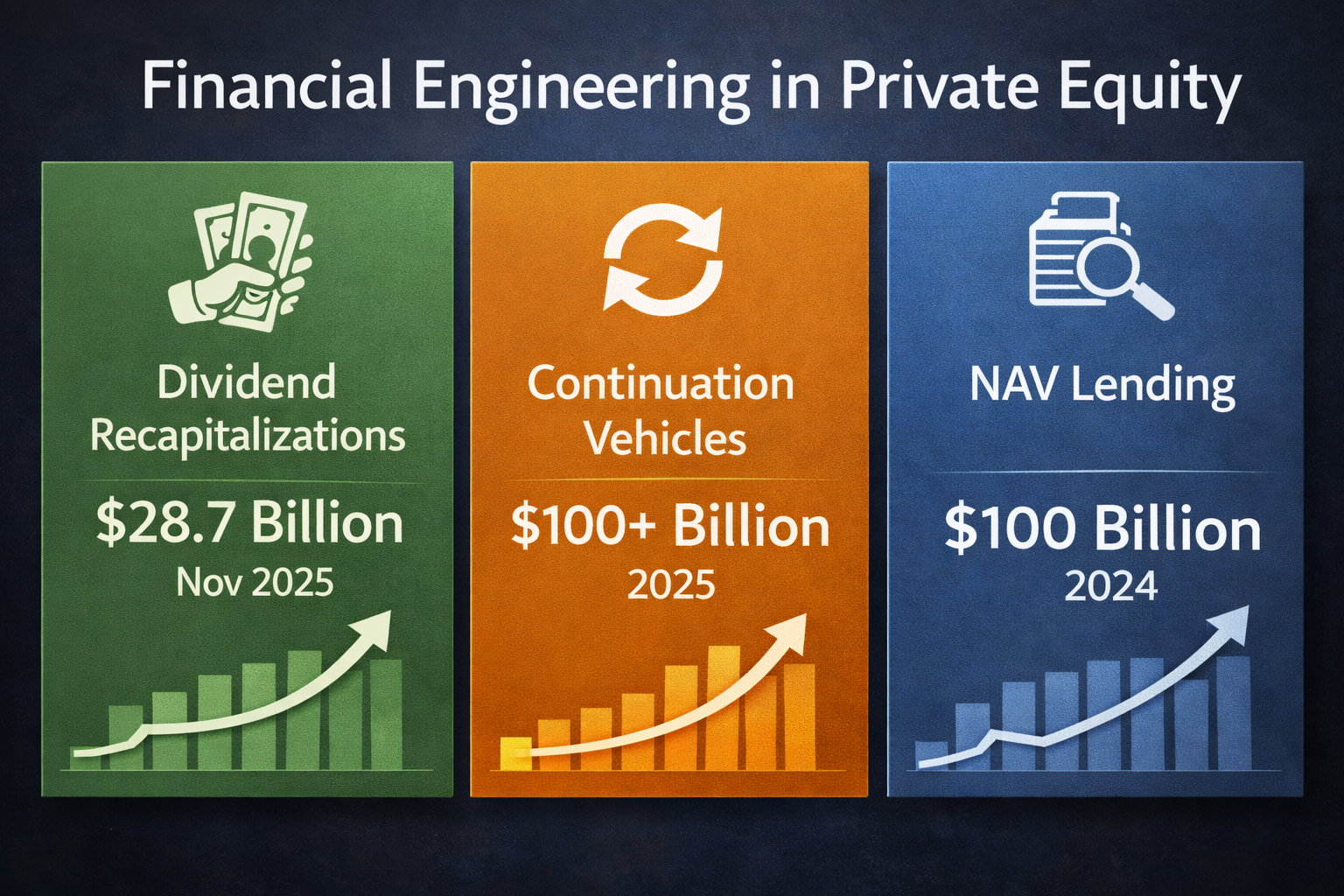

Faced with a liquidity crunch and restive investors, the industry has increasingly turned to financial engineering to manufacture distributions.

- Dividend Recapitalizations: Firms are leveraging portfolio companies to pay cash out to shareholders. Bloomberg estimates that dividend recapitalization loans reached $28.7 billion in November 2025 alone, on pace to exceed 2021 records. High-profile examples include Thoma Bravo raising $1 billion in debt on Ping Identity and $750 million on Darktrace to fund payouts.

- Continuation Vehicles: Perhaps the most controversial trend is the sale of assets from one fund to another managed by the same firm. These "continuation vehicles" accounted for one-fifth of all private equity sales in 2025, with assets in such structures swelling from $35 billion in 2019 to over $100 billion. While this ostensibly returns capital to LPs, the valuations are determined by the GP, who sits on both sides of the transaction. The risks of this circular economy are becoming evident: the Abu Dhabi sovereign wealth fund is currently suing private equity firm EMG for breach of fiduciary duty regarding a continuation sale, and companies like Wheel Pro and United Site Services have filed for bankruptcy following their transfer to such vehicles.

- NAV Lending: Funds are also taking out loans against the net asset value of their portfolios to force distributions. NAV loan volume hit $100 billion in 2024, growing at a 30 percent compound annual rate since 2019. However, the utility of this cash is questionable. Because some loans contain "recall" provisions allowing lenders to claw back proceeds, many LPs simply park the distributed cash in low-yield accounts rather than reinvesting it, rendering the distribution a formidable accounting metric but a functional nullity.

The Fundraising Feedback Loop

The lack of genuine exits has broken the cycle of capital formation. Without distributions, the metric known as DPI (distributions to paid-in capital), institutional investors cannot commit to new funds. The median fund from the 2019 vintage had distributed only 22 percent of its capital by 2024, compared to 33 percent for 2014 vintage funds at the same stage.

Consequently, fundraising is contracting. Preqin data indicates that global private equity fundraising across all strategies declined in 2022, 2023, and 2024. The industry is expected to raise less than $600 billion in 2025, a sharp drop from the $840.9 billion peak in 2023. Buyout funds are particularly hard hit, raising just $190.2 billion globally in the first half of 2025.

Outlook: A Long Road to Liquidity

The industry remains divided on the path forward. Executives at Blackstone and Ares have projected optimism for 2026, banking on an IPO resurgence and falling interest rates to clear the backlog. However, Bain & Co.’s global private equity chair offers a more sober assessment, characterizing the situation as a "5+ year problem" comparable to the aftermath of the Great Financial Crisis.

Even if the macro environment improves, digging out from under an overhang of overvalued, aging assets will be a multi-year process. Institutional allocations to alternatives have tripled from 10 percent in 2000 to 30 percent in 2025, leaving pension funds and endowments heavily exposed. Until the gap between book value and market reality closes, the liquidity squeeze will likely persist, leaving the industry to rely on debt-funded distributions and internal asset shuffles to keep the machine running.

.svg)